Stephen Laughton introduces his new book The Money Sham, recently published by Lola Books.

The Money Sham is a new and accessible macroeconomic book that dismantles piece by piece the neoliberal narrative that Burnham wants to abandon. He will fail if he sticks to fiscal rules and all the other constructs of mainstream economics. The book is aimed at all progressives and it argues that its framework and consequent prescriptions are a necessary condition for building a sustainable equitable future.

As an example of the mainstream myths that it dismantles, we can turn to the current interest rate myth, espoused by nearly all academic economists and pedalled daily on our media.

Reality: Raising interest rates does not reduce prices even for a demand-side inflation, let alone the current supply-side inflation.

Facts

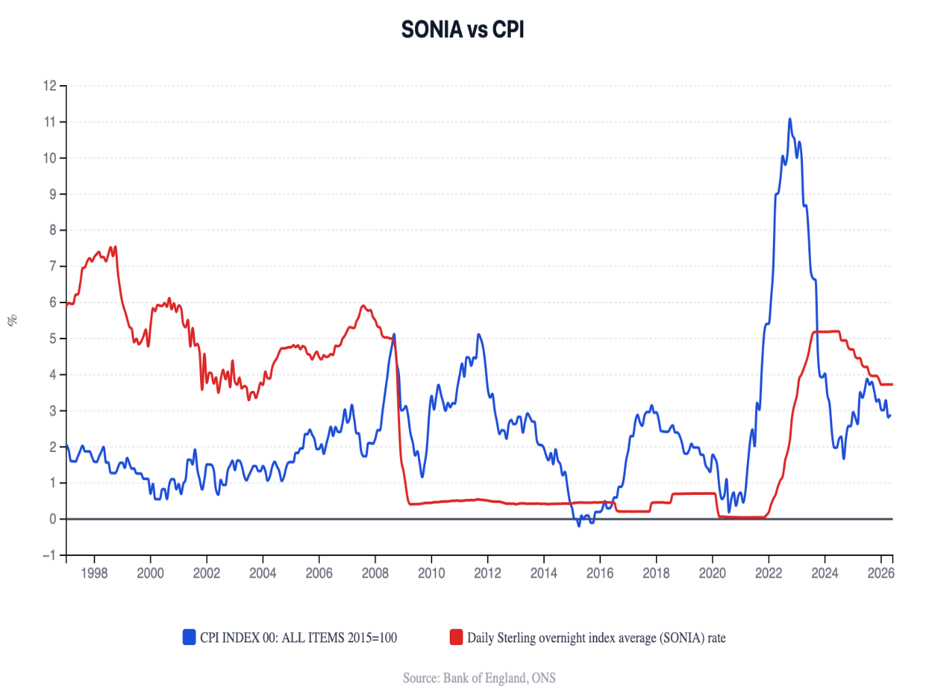

Across advanced economies over many decades, interest rates have often followed changes in the Consumer Price Index, so they cannot be determining the CPI. Over time, inflation rates tend to converge to the interest rate. In recent decades the correlation between inflation and interest rates has been positive: lower interest rates have produced lower inflation, and higher rates have produced higher inflation. As regards the UK, the chart below shows that from 1997 to 2026 the R value is -0.06, indicating no meaningful consistent relationship for the period as a whole.

SONIA vs CPI, 1997–2026 · correlation r = -0.06 · Source: Bank of England, ONS

If you look at certain years, you will see periods when interest rate rises are followed by falling prices, and some when interest rate rises precede rising prices. You can also observe interest rates flatlining after the Great Financial Crash with considerable variations in prices. You can see when CPI changes follow interest-rate changes, when they precede them, and when there is no observable relationship at all.

After Covid it is clear that supply side issues are driving prices, with interest rate policy irrelevant or counter-productive.

To support the fact that there is no consistent relationship between interest rates and inflation, Central Banks around the world have conducted studies which find that raising rates does not necessarily reduce lending. These studies, (Edwards 2021; Lane and Rosewall 2015; Melolinna, Miller and Tatomir 2018; Saleheen et al. 2017; Shah, Bunn and Melolinna 2025; Sharpe and Suarez 2015) observed that, over time, inflation rates converge towards the interest rate.

Raising interest rates is meant to stop firms investing and to stop savers spending: the savers are supposed to stop spending so as to bag the higher rates on their savings.

As detailed in The Money Sham, higher rates do not necessarily reduce investment and if they do, how does depriving the economy of investment solve a supply side inflation? Certainly, in the medium term, reduced investment will drive up prices. Even the Bank of England has recently gone some say to admitting this.

Higher interest rates give extra unearned income to those who have savings, and pass the inflationary burden on to borrowers. It’s a very neoliberal policy, that no progressive should endorse.

Supply Side Problem for Housebuilding

A key issue identified by the Labour Government and Burnham is the need to build 100,000 new homes. But due to decades of underinvestment in the workforce, in the short term this will be impossible: currently builders, due to lack of available workers, have considerable lead times before they can start a project. If customers want building work to start soon, they have to pay a higher price. To start right away, builders have to jack up prices and offer higher wages to poach existing labour. At the macro level, this does not get any more building work done, as the labour poached can only be in one site at one time.

For years young people have been encouraged to abandon the trades and gain a university degree. This policy needs to be rebalanced. To build more houses without inflation, requires lower interest rates, more investment and more government spending on investment and training. The government has the capacity to do this, if it abandons the myths of mainstream economics. It needs to adopt Real Resource Economics and break free from fifty years of economic orthodoxy

To go forward we must go back

In 1945, Beardsley Ruml of the Federal Reserve declared that “taxes for revenue are obsolete”. Keynes said simply: “Whatever we can actually do, we can afford.”

After the Second World War, with public debt above 200% of GDP, Britain created the National Health Service, maintained near full employment, and built hundreds of thousands of affordable homes. The country did not wait to “find the money”. It mobilised people, skills, materials, land, technology and political will.

Seventy years later, after astonishing advances in science and technology, with satellites orbiting the planet and billionaires competing to send rockets into space, we are told that we cannot house ourselves, cannot pay nurses properly, cannot maintain decent public services, and cannot protect people from poverty and insecurity.

Left and right repeat the same fatal phrase: “We would like to help, but we cannot find the money.” The only way progressives get elected is by promising to do nothing that might threaten those who hold power. Once in office they wonder how they became so unpopular. Their response: ‘tough decisions’ had to be made. But tough for whom?

In the 1970s, a cartel quadrupled the price of oil, the energy source on which the post-war economy depended. The resulting inflation gave the old economic doctrines their opportunity to return. The post-war consensus was dismantled. Finance was once again allowed to rule the roost. Economics, shrouded in mathematics and algebra, produced economists and politicians in thrall to ‘the markets’. Government was declared inefficient and bad. Banking deregulation was sold as liberation. Public spending was denounced as the misuse of ‘our hard-earned money’.

We have excess and squalor. The solution: somewhere there is a pot of money that can only materialise through economic growth.

The 2026 Office for Budget Responsibility assumption is that the government is like a household. It must reduce its debt. We all ‘know’ that government debt burdens our grandchildren. First, we must ‘find the money’; taxes fund spending; bond markets rule elected governments; unemployment is unavoidable; inflation is caused by excessive public spending or excessive wages; private markets, left alone, allocate resources efficiently.

Real Resource Economics rejects these doctrines and asks different questions. It begins with a simple proposition: a country like the UK is not constrained by a shortage of its own money. It is constrained by real resources: people, skills, energy, land, technology, materials, infrastructure, ecological limits and productive capacity.

The questions we should ask are not ‘Can we afford it?’ but:

- Can we do it?

- Do we have the workers, materials, technology and organisation?

- Will government spending raise or reduce inflationary pressure?

- Who gains, and who loses from the mainstream doctrine?

And why do politicians venerate an economic academia which totally failed to see the crash of 2008 and whose forecasts are consistent in being wrong? Why do they disguise regressive policy choices as ones of economic necessity?

Money is a public accounting system, not a commodity or scarce natural resource. Government spending creates financial assets. Taxation removes them. Public debt is benign: it is a record of money already spent; it is the private sector’s net savings. Private bank credit creates much of the purchasing power that drives booms, asset bubbles and crashes.

The purpose of economic policy is not to balance the government’s books. It is to balance the real economy: full employment, stable prices, decent housing, resilient public services, fair distribution, sustainable energy, productive investment and ecological survival.

And a government which chooses to, can control the bond markets. For over twenty-three years the UK government used a tap system to control them. Free marketers proclaimed this was ‘financial repression’ and the markets must be set free. And from 1991 to 1998 so they were and we can see the results. More recently, the Japanese government, albeit for the wrong reasons, has shown that a sovereign government can permanently control the yield curve by buying bonds.

The left should not grant the bond markets a power they do not deserve and which serves no purpose, apart from enriching traders and leaving pension funds at the mercy of a silly government policy of raising interest rates to combat inflation.

Real Resource Economics reasserts the post-war lesson: whatever we can actually do, we can afford.

For more information, see The Money Sham and Real Resource Economics.

Stephen Laughton Dip Econ/ MA Econ has been in the Labour Party since 1981. He was the Political Education Officer of Bournemouth East and Bournemouth West Labour for several years. He is a member of Momentum. Recently he has devoted his time to economics, and remains an independent philosophical economist, who believes current economic wisdom is deeply flawed and that centrist politicians who follow it are paving the way for their own demise.